ASML Misses On Orders As CEO Warns Of Trade War; Analysts Call Results “Disappointing”

Nasdaq 100 futures declined 1.5% early Wednesday, driven by renewed pressure on semiconductor stocks. Nvidia fell about 6% in pre-market trading following the Trump administration’s move to block exports of its H20 AI chips to China. Meanwhile, shares of ASML Holding slid around 5% in European trading after the company delivered a weaker-than-expected earnings report, casting a dark shadow over the near-term outlook for the global semiconductor industry amid mounting economic pressures from the trade war.

Dutch chip equipment maker ASML, which designs and manufactures lithography systems for Intel and Taiwan Semiconductor Manufacturing, reported bookings of 3.94 billion euros in the first quarter, missing the average analyst estimate tracked by Bloomberg of 4.82 billion euros. ASML pointed out that order intake for EUV machines is a “lumpy” metric and doesn’t accurately reflect momentum in the industry.

The key takeaway for the 1Q25 earnings: ASML delivered mixed results, with better-than-expected margins and earnings offset by a sharp decline in bookings. The results suggest solid near-term performance but growing demand uncertainty as the artificial intelligence bubble was ‘DeepSeeked‘ earlier this year, plus mounting macroeconomic headwinds from deepening trade wars already filtering into main shipping channels between Asia and the U.S.

Here’s a snapshot of the first quarter earnings:

Bookings EU3.94 billion, -44% q/q, estimate EU4.82 billion (Bloomberg Consensus)

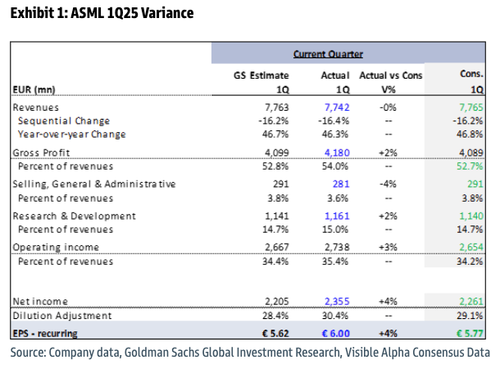

Net sales EU7.74 billion, -16% q/q, estimate EU7.75 billion

- Net system sales EU5.74 billion, estimate EU5.69 billion

- Net service & field operation sales EU2.00 billion, estimate EU2.1 billion

Gross margin 54% vs. 51.7% q/q, estimate 52.5%

R&D expenses EU1.16 billion, estimate EU1.14 billion

Operating income EU2.74 billion, estimate EU2.65 billion

Operating margin 35.4%, estimate 33.9%

Net income EU2.36 billion, -13% q/q, estimate EU2.24 billion

Cash and other EU9.10 billion, -29% q/q, estimate EU12.21 billion

Total lithography systems sold 77 units, estimate 100.62

ASML CEO Christophe Fouquet said in the company’s quarterly earnings statement that ongoing customer discussions reinforce the company’s expectation that both 2025 and 2026 will be years of growth.

“However, the recent tariff announcements have increased uncertainty in the macro environment,” Fouquet warned.

ASML’s 2025 financial guidance remains unchanged, but that could change if trade wars deepen…

Second Quarter Forcast:

-

Sees net sales EU7.2 billion to EU7.7 billion, estimate EU7.66 billion

-

Sees gross margin 50% to 53%, estimate 52.3%

-

Sees R&D expenses about EU1.2 billion, estimate EU1.16 billion

Full Year Forecast:

-

Still sees gross margin 51% to 53%, estimate 52.1%

-

Still sees net sales EU30 billion to EU35 billion, estimate EU32.59 billion

Commenting on the results, Citi analyst Andrew Gardiner told clients that ASML’s first-quarter orders were “disappointing,” with tariff-related uncertainty “clouding” the outlook. However, he noted that the reaffirmed full-year guidance and the company’s expectation of continued growth into 2026 offer investors a partial sigh of relief.

Barclays analyst Simon Coles told clients that ASML would need to hit 3 to 5 billion euros of orders each quarter for the next 3 to 5 quarters to hit consensus expectations: ”This seems manageable but our worry is two major customers are unlikely to be ordering significantly any time soon.”

Here are Goldman analysts Alexander Duval and Anant Jakhar’s first take on the first quarter results:

ASML’s 1Q25 revenue was in-line but EBIT was above Visible Alpha Consensus Data, driven by higher gross profits which benefited from a higher share of 3800E tools in the mix (which have higher ASP) and customer specific performance target rewards. The company’s bookings figure in 1Q was €3.9bn, (down qoq from a very strong 4Q24 order intake of €7.1bn and below Visible Alpha Consensus Data of c.€4.8bn), including €1.2bn of EUV orders (below cons estimate of €1.6bn). As such, we note that the 1Q25 order intake of €3.9bn is higher than the order run-rate needed (c.€3-4bn) to hit the 2026 cons estimate. Importantly the company shipped another High NA tool in the quarter which could be taken positively by investors. The company acknowledged macro uncertainty but sees AI as the main driver of its market. Furthermore, the company stated that based on its discussions with customers it sees both 2025 and 2026 to be growth years. The company introduced its 2Q25 net sales guidance of around €7.2-7.7bn and expects 2Q25 gross margins to be around 50-53% (a wider range to reflect macro uncertainty) implying revenue/gross profit/EBIT that is 4%/6%/10% below cons. Further, ASML reiterated its 2025 guidance and expects sales of €30-35bn, with gross margins of 51-53%. Additionally, we note that ASML’s 2Q25 guide for GM includes a certain degree of dilution from ramp of high NA but the company remains on track to deliver its FY25 GM target as it expects 3800E to become the main Low NA tool being shipped to customers.

In terms of end market trends, ASML expects continued strength in advanced Logic, with customers ramping 2nm technology nodes, strong memory at same level as last year, and growth in installed base management driven by more EUV. The company believes the Memory market will remain robust at the same level as last year, as confirmed by customer activity. Furthermore, we note ASML’s growing Installed Base, driven by a stronger mix of EUV versus DUV. Finally, the company reiterated its LT 2030 revenue and GM guidance. More broadly, we expect investors to seek more colour of the recent tariffs on semiconductor equipment and end market demand, latest expectations for order intake from Foundry/leading-edge customers, demand dynamics in the trailing-edge end markets. Reiterate Buy.

Goldman’s view:

We expect an initial mixed reaction in the shares, in light of a beat on the current quarter KPIs versus consensus, and commentary around 2025/26 to be growth years offset by below cons order intake as well as below-cons 2Q25 guide. That said, we note that ASML has underperformed by 6% vs EU Tech in the last 3 months, and is down 11% abs YTD. We expect investors to seek more colour of the recent tariffs on semiconductor equipment and end market demand, latest expectations for order intake from Foundry/leading-edge customers, demand dynamics in the trailing-edge end markets.

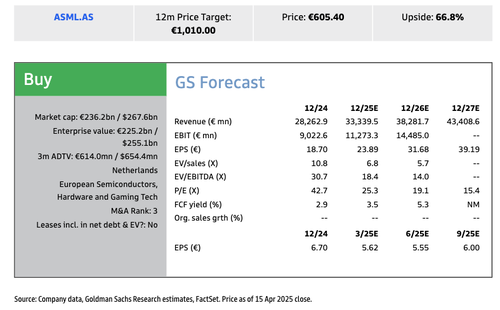

Goldman = Buy-Rated ASML:

We are Buy rated on ASML with a 12-month price target of €1,010 based on a 32x CY26E P/E multiple. Key risks to our view and price target include EUV delays, capex cyclicality and unfavourable market share shifts.

More institutional commentary on the first quarter results and outlook:

Stifel (hold)

2Q guidance is soft, below consensus with a 10% miss at the Ebit level, says analyst Juergen Wagner

Both EUV and overall orders missed estimates for 1Q; 2025 guidance was confirmed, but “with a tariff disclaimer”

With 2Q guidance a miss, the year now looks increasingly back- end loaded

Morgan Stanley (equal-weight)

Net bookings suggest that only six low-NA EUV tools were ordered in the March quarter, showing weakness, says analyst Lee Simpson

Implied DUV bookings of €2.7b confirms a decent China order book

Firm still sees AI as a key demand driver and has seen demand for 2026 starting to solidify, but it also notes potential tariff impact. Its weak 2Q guidance reflects some of this caginess

ASML’s shares fell 5% to 575 euros in the early afternoon trading hours in Europe. Shares are down 42% since peaking at around 1,000 euros in mid-July last year.

The key question is whether the deepening trade war will derail the global race for AI, or if the U.S. and China can reach a resolution in the near term to defuse the trade war bomb that could sent the global economy into a downward spiral.

Tyler Durden Wed, 04/16/2025 – 08:20

Source: https://freedombunker.com/2025/04/16/asml-misses-on-orders-as-ceo-warns-of-trade-war-analysts-call-results-disappointing/

Anyone can join.

Anyone can contribute.

Anyone can become informed about their world.

"United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

Before It’s News® is a community of individuals who report on what’s going on around them, from all around the world. Anyone can join. Anyone can contribute. Anyone can become informed about their world. "United We Stand" Click Here To Create Your Personal Citizen Journalist Account Today, Be Sure To Invite Your Friends.

LION'S MANE PRODUCT

Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules

Mushrooms are having a moment. One fabulous fungus in particular, lion’s mane, may help improve memory, depression and anxiety symptoms. They are also an excellent source of nutrients that show promise as a therapy for dementia, and other neurodegenerative diseases. If you’re living with anxiety or depression, you may be curious about all the therapy options out there — including the natural ones.Our Lion’s Mane WHOLE MIND Nootropic Blend has been formulated to utilize the potency of Lion’s mane but also include the benefits of four other Highly Beneficial Mushrooms. Synergistically, they work together to Build your health through improving cognitive function and immunity regardless of your age. Our Nootropic not only improves your Cognitive Function and Activates your Immune System, but it benefits growth of Essential Gut Flora, further enhancing your Vitality.

Our Formula includes: Lion’s Mane Mushrooms which Increase Brain Power through nerve growth, lessen anxiety, reduce depression, and improve concentration. Its an excellent adaptogen, promotes sleep and improves immunity. Shiitake Mushrooms which Fight cancer cells and infectious disease, boost the immune system, promotes brain function, and serves as a source of B vitamins. Maitake Mushrooms which regulate blood sugar levels of diabetics, reduce hypertension and boosts the immune system. Reishi Mushrooms which Fight inflammation, liver disease, fatigue, tumor growth and cancer. They Improve skin disorders and soothes digestive problems, stomach ulcers and leaky gut syndrome. Chaga Mushrooms which have anti-aging effects, boost immune function, improve stamina and athletic performance, even act as a natural aphrodisiac, fighting diabetes and improving liver function. Try Our Lion’s Mane WHOLE MIND Nootropic Blend 60 Capsules Today. Be 100% Satisfied or Receive a Full Money Back Guarantee. Order Yours Today by Following This Link.

| Online: | |

| Visits: | 1,689,140,660 |

| Stories: | 8,395,297 |

Whistler Blowers, Insiders